Have you heard of the Washington Cares Fund? If you haven't, it's the first state run and funded Long-Term Services & Supports program. Originally signed in 2019 by Governor Jay Inslee, as of January 1st, 2025, Washington State Residents who need long-term care may be able to claim benefits (based on needing help with 3 of 10 ADLs) from the state and receive a benefit of up to $100 per day up to a maximum benefit of $36,500. Undoubtedly for many families these benefits are going to welcomed and helpful. But, of course, someone has to pay for the program.

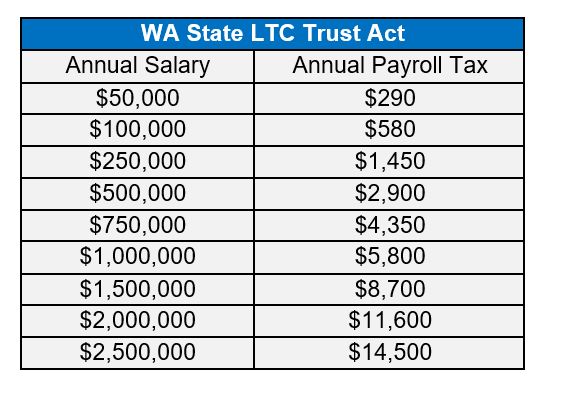

How is Washington State paying for this? By instituting a payroll tax on W-2 Employees of .58% of payroll. Here's an example of the annual payroll tax at different income levels:

Bonus income is also considered W-2 wages, so for high earners the tax can increase quickly. The tax is mandatory for W-2 employees while self-employed people may choose to opt into the plan and payroll tax.

In addition to the self-employed, who else can avoid the payroll tax? Well, the legislation wisely allows people who have planned ahead and already own LTC Insurance to apply for a payroll tax exemption from their employer beginning in October. Consider this a "private" option for long-term care insurance.

Under current rules in order to opt-out of the payroll tax, Washington state residents will need to secure LTC Insurance coverage by November 1st of 2021.

What qualifies as LTC Insurance for the purposes of exemption? Unfortunately, it is not clear EXACTLY what coverage will guarantee exemption from the tax. I'm sure people would love to know what the so called "safe harbor" rules of plan design are but the current legislation is vague. For those who want to find the legislative language of what qualifies as LTC Insurance it can be found here.

Many traditional LTC policies and hybrid policies with tax-qualified (7702B) benefits should qualify for the exemption. For example, buying a policy that has benefits similar to the current cost of home care, inflation protection, and a three year benefit period should qualify.

A problem could arise for Washington residents who attempt to buy "minimum" coverage.

Our company recently had a young executive who made $500,000 per year apply for coverage of $1,500 per month that lasted two years, or a total benefit of $36,500 - no inflation protection was added. The total premium for this plan? $228 per year!. Compare that to the $2,900 annual payroll tax he would be required to pay without LTC coverage. It's pretty obvious that this purchase is being made to avoid the payroll tax - tax that the state depends on for the solvency of the public LTC program. If the the payroll tax doesn't support the program the payroll tax could increase over time.

In addition to the state being concerned about opt-outs, the insurance carrier issuing the policy will be incurring all the cost involved with underwriting and placing this policy (not to mention the low agent compensation). They will struggle to earn money off this applicant, especially if the policyholder lapses coverage after a few months to try and escape the tax and premiums.

The old saying stands - if it is too good to be true it probably is. High income earners should do the right thing and buy a decent private LTC plan if they'd like to avoid the payroll tax. If they own a Health Savings Account they can even pay premiums with pre-tax dollars. They will end up with substantially more coverage than the state option as well.

People often wonder if their tax dollars will be "wasted". The good thing about a payroll tax funded LTC plan is that we know the people who will benefit - people needing care and their caregivers. Let's hope the Washington State plan will build awareness of the care crisis so that we all can respond to it.

You can download a guide to the Washington State Program here

-CMYK.png?width=200&name=LifeSecureLogo(F)-CMYK.png)